In this third installment of the “A Year of Health” series, we take a look at financial health.

Finances are the number one cause of stress, according to the insurance company Blue Cross/Blue Shield. From millennials to boomers, people of all ages are experiencing stress over finances such as saving for retirement, paying bills or putting food on the table.

The year 2020 not only took a toll on our physical and mental health, for those that experienced layoffs or furloughs, the pandemic had major effects on their financial health, as well.

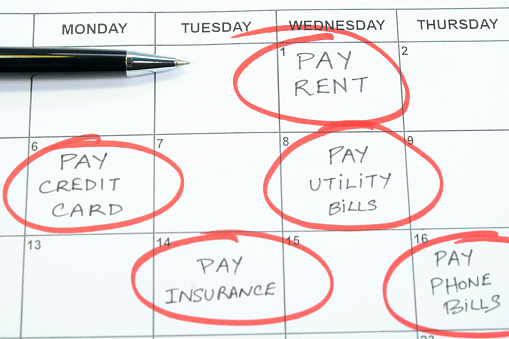

According to the financial website, Nerd Wallet, while credit card balances carried from month to month dropped by more than 6% in 2020, other types of debt — mortgages, rent, car payments, student loans — increased from 2019 to 2020.

The website reports that nearly 1 in 7 Americans (14%) say their financial situation has gotten better since the onset of the pandemic, with 42% reporting that their financial situation has gotten worse.

Those that are struggling have tapped into their savings, borrowed from retirement accounts and added more debt through credit cards, the website said.

“There’s hope for the next year, thanks to positive vaccine news, but it’ll take time for some Americans to bounce back from months of financial instability.

There’s no question that paying down debt is an uphill battle. It takes time, sacrifice and patience. However, it can be done.

“The key to any personal development, including eliminating debt, is adopting the right mindset, building a solid plan and then following through on action items,” Joshua Fulenwider said.

Fulenwider is a former commercial banker, author of the book “What We Should Teach Our Children About Money,” and business owner. He offers some tips and tricks that people can use to help pay down their debt and get on track.

Before you begin

The first thing people should think about is the “why” of wanting to pay off debt.

Are you tired of the stress that being in debt causes or do you want to eliminate debt so that you can start saving for retirement or to purchase a house?

Maybe you want to finally take that vacation to Alaska you’ve dreamed about or go back to school to get your degree.

Whatever your “why,” fleshing this out is an important step in the debt elimination process.

“Defining why you want to eliminate debit will help you stay motivated and focused,” Fulenwider suggested. “Write it down and revisit it often.”

Like with any goal, being accountable for your actions is one of the keys to success. If you are married or have a partner, involving them in the process will help with accountability for the household. If you are single, try to find a mentor that can help guide you based on their experience. Both options can help keep you on track.

The third thing you should do prior to paying off debt is make a plan.

“Good intentions aren’t enough,” Fulenwider said. “Determine your step-by-step plan to achieve your goal. Write this down too so that you can refer to it and measure your progress.”

Tips and tricks to use in your plan

You have narrowed down your “why,” you’ve got support to hold you accountable and you’re ready to start formulating a plan.

So where do you start?

Fulenwider advises stop making more debt as the first step in your plan.

If you find yourself getting into trouble with credit cards, cut them up and go back to using cash, he said. Also, avoid purchasing anything that needs to be financed such as a car or appliance.

“I discourage debt consolidation loans as well. Often these loans don’t reduce interest rates, they have fees to set up and you can always go charge more purchases on the credit cards you just paid off,” Fulenwider explained. “There are times when these are appropriate, but use them with caution.”

Making your payments on time will help avoid late-fees, which can rack up debt. Also, don’t charge more than your limit, which can also cause fees to accrue. Late and/or overdraft fees also can take a toll on your credit score.

Fulenwider also advises looking at your monthly expenses to see where you can make cuts. Things like unused gym memberships or an overabundance of steaming services are small drains on your finances that can add up.

“Look at the last three months of your bank statements to see what money are spending and if you can reduce or eliminate any of it,” he said. “Replacing one meal a week that you normally get at a fast food restaurant can save you almost $40 a month per person.”

Instead of using the “shotgun approach” where you throw money at all of your bills at once, Fulenwider suggests using the “snowball effect” and focus on paying off your smallest bill first by using as much of your extra money as you can to pay it off, while paying the minimum on the larger bills.

“Once that debt is paid off, you will have even more money to tackle your next smallest debt,” he explained. “Each time you pay off a debt, you have more money each month to pay off the next one.”

Lastly, build a reward system into your plan to create an incentive to keep going.

“When you get a debt paid off, take a month off from your ‘snowball’ repayment plan and use the money you’ve freed up to treat yourself,” Fulenwider said. “If it’s the first debt you’ve eliminated, you might have only $50 to treat yourself. Buy by your third or fourth eliminated payment you might be able to buy yourself a new TV. This is a time for you to celebrate your success.”

You’ve eliminated your debt, so now what

Yay! You’ve got yourself out of debt and have extra money.

Instead of going on spending sprees, use that extra money to build up your savings account for emergencies or the next vehicle you will need to purchase. You can also look into investing some of that extra money into a retirement account such as a Roth IRA or upping your contribution to your 401K plan.

Whatever you do, avoid getting back into debt.

“Sometimes debt is nearly unavoidable, such as when purchasing a home,” Fulenwider said. “However, purchasing smaller things shouldn’t cause you to go back into debt. If you start using credit cards again, make sure you pay them off at the end of the month.”

If you find yourself struggling again, it’s time to take a step back and look at your finances and budget and repeat your plan.

“Eliminating debt relives a ton of financial stress,” Fulenwider said. “Having money in the bank bring even more peace of mind.”

For more tips and tricks to paying off debt, go to http://bit.ly/3tDLUHw.

To check out Fulenwider’s book, “What We Should Teach Our Children About Money,” or for more information on finances, business and networking, go to www.JoshuaFulenwider.com.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}