The Indian financial ecosystem has seen rapid progress and technological innovations in the past decade. They range from digital payment and credit disbursal platforms, to provision of competitive insurance and investment products.

The success of these innovative platforms and services is reflected in the flourishing user base. Take the Unified Payments Interface (UPI) for example: in 2019, payments through UPI overtook card payments in the country.

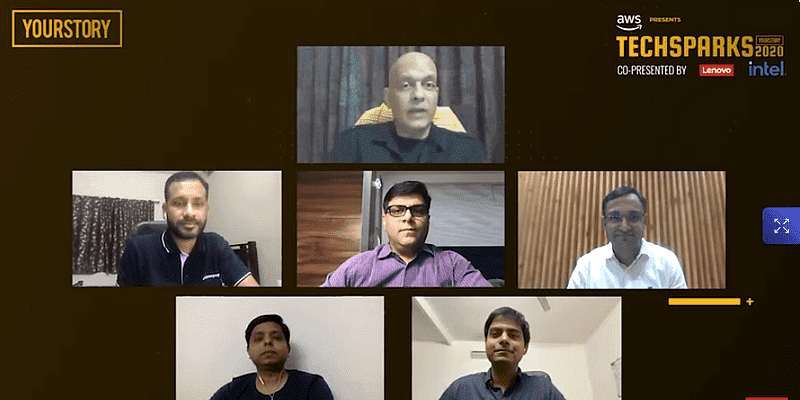

A distinguished panel of industry leaders at TechSparks 2020 addressed the emerging opportunities and tech transformations that will define the future of this key sector. The speakers were Saurabh Tiwari, CTO, PolicyBazaar; Raju Shetty, Head of Engineering, Razorpay; Mayank Kachhwaha, Co-founder and COO, IndiaLends; Vijay Aggarwal, CTO, BharatPe; and Suvig Sharma, Director APAC, MongoDB for India and ASEAN.

Here are some key takeaways from the wide-ranging discussion, on how tenacious fintech players are leveraging technology architectures and customer-centricity to build trust in their markets.

Industry trends

The panelists shared insights on industry trends in insurtech, credit space, B2B markets, and cybersecurity.

For example, the D2C model has opened up new opportunities in insurtech, according to Saurabh of PolicyBazaar. Scalable enterprise software makes it possible to offer more customer-centricity in offerings, and digital payments make the engagement smoother.

A data management approach enables customisation and personalisation of products for a broad user base. SaaS models for insurtech that bundle marketing, sales and customer service will boost industry efficiency even more, Saurabh added.

Affordability of financial products is a big concern in an emerging economy like India, Raju of Razorpay explained. More innovation is needed for small ticket and small duration loans. New business models and channels will open up for financial inclusion, and online video and voice are trends to watch.

Purchasing parity dips after the 150 million user mark. An estimated 80 percent of the market in India is still untapped, according to Raju.

India is still more of a “do it for me” market than a “do it yourself” play, he added. Issues like cross-border services and fraud insurance are not yet fully solved. There is lots of potential for B2B offerings.

The COVID-19 pandemic impact led to headwinds and tailwinds in India’s financial services sector. Much activity stopped during the lockdown, and there continues to be job loss. Signs of economic weakness are a big worry, observed Mayank of IndiaLends.

But there is a big change in terms of fulfilment and regulations. “There is change in both the customer and lender side, as more loans are beginning to originate digitally,” he said. Regulation is also becoming supportive of the fintech sector.

For example, there is lots of work happening at the ecosystem level. UPI’s impact on payment has been game-changing, Mayank said. Data capabilities can help understand and include customers at the margin. “In a couple of years, big effects will be seen, and large banks will change,” he predicted.

Regulation plays an important role in nurturing growing sectors like fintech, but there is a lot more to be done, suggested Vijay of BharatPe. “An important role for regulators is creating healthy competition between existing players, and enabling entry of new players,” he said.

He cited UPI is a good example of this, via interoperability of payment options. Mobile number portability had a big impact in the telecom sector, Mayank recalled. Enabling infrastructure can smoothen KYC even more, as seen in how Aadhaar facilitated easier compliance.

Cybersecurity is a very important concern for fintech, and can incur huge costs annually, observed Suvig of MongoDB. This assumes particular importance with the rise of the public cloud and billions of connected device.

“The surface area for cyber-attacks has dramatically increased, and it is getting more sophisticated,” Suvig cautioned, pointing to ransomware as an example. Fintechs have to be able to detect and prevent fraud without disrupting service for a genuine customer.

In addition to traditional approaches like firewalls, a data-centric approach towards cybersecurity is needed. This will involve collating an array of internal and external datasets and processing them in real-time, Suvig explained.

Behavioural analytics and machine learning need to be combined to detect and prevent fraud – by looking for anomalies in user behaviour, for example. This will involve rethinking the underlying data management technologies for authentication, identity, and encryption.

The data advantage

Insights from big data, analytics, and technologies like artificial intelligence (AI) and machine learning (ML) are propelling fintech players to the next level of evolution.

The work-from-home (WFH) paradigm during the pandemic increased the need for fraud and anomaly detection tools, observed Saurabh of PolicyBazaar. Customer contact centers used voice analytics to understand user intent and pick up potential anomalies in behaviour.

Mayank of IndiaLends also shared his company’s experience in using voice analytics at their large call centre. Insights from unstructured data were used to build better voice bots, increase sales, and build risk models.

Learnings were gleaned from voice analytics as well as clickstream data. Data insights helped deciding the right product to offer to the right customer at the right time.

Data analytics has helped ecommerce merchants reduce cart abandonment rates, according to Raju of Razorpay. Two-factor authentication is not always needed, and the interaction can be made smarter for regular customers based on user profile analysis.

Data capabilities improve app interactions via user prompts as well as internal alerts, explained Vijay of BharatPe. Effective customer journey analysis helps tweak and optimise products, and customise a range of offerings.

Data insights can enable financial access to those who are not getting formal banking services, an even more important consideration during COVID times. Data-based employee engagement can also be leveraged internally, according to Vijay – for example, via surveys to track levels of pride and happiness in employees.

In sum, data and AI innovation can greatly help detect fraud, improve productivity, personalise offerings, and create new lines of business in fintech, according to Suvig of MongoDB. He cited the example of a Bengaluru fintech startup addressing the underserved student market.

There are a lot of possibilities opening up, but integration and interoperability also mean more security is needed, he cautioned. Data capabilities help take better care of existing customers as well as identify new whitespaces for revenue streams.

Fintech companies’ agility is a strong advantage in this regard. “There is a growing partnership between traditional players with massive amounts of data, and fintech players who have speed, innovation and agility on their side,” Suvig signed off.

TechSparks – YourStory’s annual flagship event – has been India’s largest and most important technology, innovation, and entrepreneurship summit for over a decade, bringing together entrepreneurs, policymakers, technologists, investors, mentors, and business leaders for stories, conversations, collaborations, and connections that matter. As TechSparks 2020 goes all virtual and global in its 11th edition, we want to thank you for the tremendous support we’ve received from all of you throughout our journey and give a huge shoutout to our sponsors of TechSparks 2020.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Why are there so many Arduino clones but barely any Raspberry Pi clones? : opensource